Each year the 193 member states of the United Nations General Assembly vote on dozens of resolutions, earnestly setting the world to rights. Last month, for example, they voted in favour of reducing space threats, eradicating rural poverty and combating dust storms, among other things. The votes count for little. The assembly’s resolutions are not legally binding. Its budgetary powers are small. And it has as many military divisions as the pope.

But for scholars of international relations, these votes have long provided a handy, quantitative measure of the geopolitical alignments between countries. More recently, economists have also turned to them. Owing to the trade war between America and China, Russia’s invasion of Ukraine, the conflict in Gaza and recent blockades in the Red Sea, geopolitics has become impossible for dismal scientists to ignore. Although their models of trade and investment typically give pride of place to the economic size of countries and the geographic distance between them, they are now considering “geopolitical distance” as well.

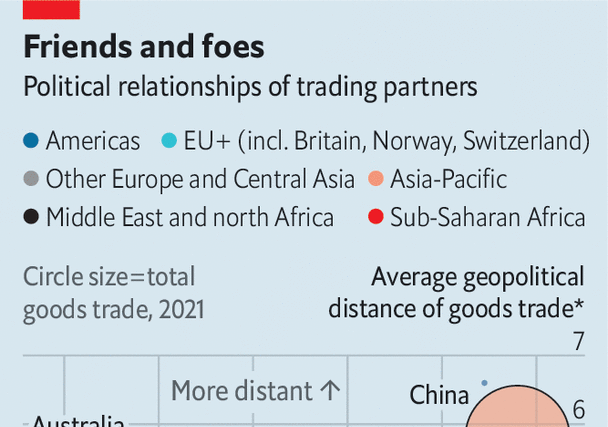

The latest such study was published this month by the McKinsey Global Institute, a think-tank attached to the consultancy of the same name. By analysing countries’ votes on 201 of the higher-profile resolutions between 2005 and 2022, McKinsey was able to plot countries’ geopolitical stances on a scale from zero to ten. America stands at one end of the spectrum, labelled zero. At the other end is Iran at ten. In between are countries like Britain at 0.3, Brazil at 5 and China at 9.6.

The authors use this measure to provide a new perspective on each country’s trade. As well as measuring the average geographical distance that a country’s trade must travel, they also calculate the geopolitical distance it must traverse. In a hypothetical world in which half of Iran’s trade was with America and half with Brazil, its trade would cover a geopolitical distance of 7.5.

Their results are illuminating. European countries trade mostly with one another. As a consequence, their trade for the most part flows to their friends and neighbours. Things are rather less comfortable for Australia, however. It must trade with countries that are both geopolitically and geographically remote.

America is somewhere in between. Thanks in part to its continental size, it has few prosperous neighbours. Less than 5% of global GDP is generated by countries within 5,000km of America, as McKinsey points out. Its trade travels almost 7,200km on average, compared with 6,600km for China’s trade and a global average of less than 5,200km. Yet in the diplomatic realm, the world is not so far away. The geopolitical distance America’s trade must cover is only a little above the global average. It is far shorter than the diplomatic distances bridged by China. Indeed, China’s trade covers a greater geopolitical gap than that of any of the other 150 countries in McKinsey’s data, bar Nicaragua, which resents America, but is doomed to do business with it.

The study finds some early evidence of “friendshoring”. Since 2017, America has managed to shorten the geopolitical distance covered by its trade by 10%, on McKinsey’s scale. It has, for example, sharply curtailed imports from China, although some of the goods it now buys from other countries, such as Vietnam, are full of Chinese parts and components. China has also reduced the geopolitical distance of its trade by 4%, although that has required it to trade with countries farther afield geographically.

Yet the report identifies several limits to this trend. Much of the trade countries carry out with ideological rivals is trade of necessity: alternative suppliers are not easy to find. McKinsey looks at what it calls “concentrated” products, where three or fewer countries account for the lion’s share of global exports. This kind of product accounts for a disproportionate share of the trade that spans long geopolitical distances. Australia, for example, dominates exports of iron ore to China. Likewise China dominates exports of batteries made from neodymium, a “rare-earth” metal.

The attempt to reduce geopolitical dangers may also increase other supply-chain risks. Friendshoring will give countries a narrower range of trading partners, obliging them to put their eggs in fewer baskets. McKinsey calculates that if tariffs and other barriers cut the geopolitical distance of global trade by about a quarter, the concentration of imports would increase by 13% on average.

For countries in the middle of the geopolitical spectrum, friendshoring has little appeal. They cannot afford to limit their trade to other fence-sitters, because their combined economic clout is still too small. Countries that score between 2.5 and 7.5 on McKinsey’s scale—a list that includes rising economies such as Brazil, India and Mexico—account for just one-fifth of global trade. To avoid falling between two stools, they must seek to trade across the geopolitical spectrum, just as they do now.

Friendshoring has limits for China as well. There are simply not enough big economies in its geopolitical orbit to compensate for reduced trade with unfriendly Western trading partners. For China, then, friendshoring is more about replacing rivals and antagonists with more neutral parties among the non-aligned world, such as in Central Asia and the Middle East.

Check mate

In studying how trade might contort itself along geopolitical lines, the McKinsey study assumes that the lines themselves remain fixed. But as the report freely admits, that might not be the case. The invasion of Ukraine and the conflict between Israel and Gaza is already causing new divisions and allegiances. It is conceivable that non-aligned countries might move closer to China politically, as China embraces them economically. Certainly, by spurning Chinese trade and investment, the West would give China added incentive to ingratiate itself with the rest of the world. After all, there are two ways to shorten the geopolitical distance of trade: trade more with friends or make more friends to trade with. ■

Read more from Free exchange, our column on economics:

What economists have learnt from the post-pandemic business cycle (Jan 17th)

Has Team Transitory really won America’s inflation debate? (Jan 10th)

Robert Solow was an intellectual giant (Jan 4th)

For more expert analysis of the biggest stories in economics, finance and markets, sign up to Money Talks, our weekly subscriber-only newsletter

The Most Read

Сryptocurrencies

Bitcoin and Altcoins Trading Near Make-or-Break Levels

Financial crimes

Thieves targeted crypto execs and threatened their families in wide-ranging scheme

Financial crimes

Visa Warning: Hackers Ramp Up Card Stealing Attacks At Gas Stations

News

Capitalism is having an identity crisis – but it is still the best system

Uncategorized

The 73-year-old Vietnamese refugee is responsible for bringing Sriracha to American consumers

Uncategorized

Electric Truckmaker Rivian, Backed By Amazon, Ford, Raises Whopping $1.3 Billion