For financial markets the Holy Grail is a perfect leading indicator—a gauge that is both simple to monitor and consistently accurate in foretelling the future. In reality, such predictive perfection is unattainable. It is often hard enough to grasp what is happening in the present, let alone the future. A perfect real-time indicator would thus be a potent goblet of knowledge, if not quite the Holy Grail, for investors and analysts to drink from. Recently they have turned their attention towards one impressive candidate: the Sahm rule.

Developed by Claudia Sahm, a former economist at the Federal Reserve, in 2019, the rule would have been capable of identifying every recession since 1960 in its early stages, with no false positives. This is no mean feat given that the body which officially declares whether the American economy is in recession sometimes needs a full year of data. The Sahm rule, by contrast, typically needs just a few months.

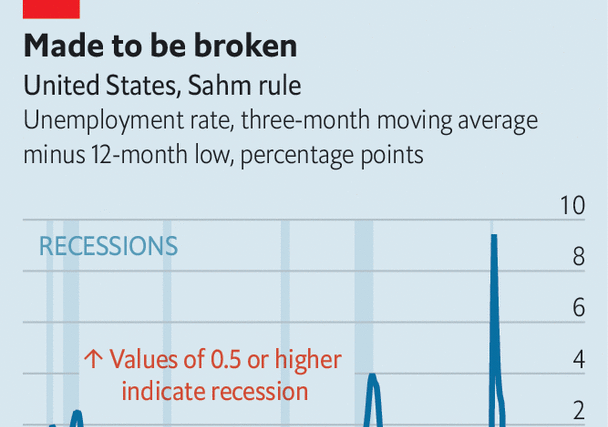

Like all good rules, it is parsimonious. If the unemployment rate increases by half a percentage point from its trough of the past 12 months, the economy is said to be in a recession. To smooth out the figures, which jump around, both the current unemployment rate and the trough are measured as three-month moving averages. At present the Sahm indicator stands at 0.33 percentage points. It would not take much for it to reach the half-point mark. If the unemployment rate, which hit 3.9% in October, rises to 4.0% this month and 4.1% next month, the economy would, according to the Sahm rule, be in a recession.

What about in reality? As Ms Sahm herself is quick to point out, her rule describes an empirical regularity, not an immutable law. What is more, the post-pandemic economy may have fostered the exact kind of conditions that violate this regularity. During downturns companies fire workers, and the layoffs typically go well beyond the Sahm rule’s half-point line.

This time, though, the increase in the jobless rate appears to have been driven less by a reduction in demand for workers and more by an increase in their supply. The American labour force, including both people in work and looking for jobs, has expanded by nearly 3m, or 1.7%, since the end of last year. During that same time the number of jobs has increased by about 2m, or 1.2%. “If workers come back and the jobs haven’t caught up with them, the unemployment rate can drift up,” says Ms Sahm. “But then as the jobs catch up, the unemployment rate doesn’t spiral upwards.”

For Ms Sahm the sudden fame of her measure has brought with it an additional wrinkle. She has had to grapple with the world taking her rule in a different direction from her initial intent. Ms Sahm was not trying to get into the forecasting business, much less into timing financial markets. Rather, she wanted to come up with a benchmark for triggering automatic payments to individuals in order to insulate them from a recession. “Many people have asked me if we are going into a recession,” she says. “Almost no one has asked me what policymakers can do about it.”

Considering the paralysis in Congress, it is a fair bet that policymakers will not do much of anything if unemployment continues to rise in the coming months. So Ms Sahm is now in the curious position of rooting against her own rule, and hoping that America skirts a recession. ■

The Most Read

Сryptocurrencies

Bitcoin and Altcoins Trading Near Make-or-Break Levels

Financial crimes

Thieves targeted crypto execs and threatened their families in wide-ranging scheme

Financial crimes

Visa Warning: Hackers Ramp Up Card Stealing Attacks At Gas Stations

News

Capitalism is having an identity crisis – but it is still the best system

Uncategorized

The 73-year-old Vietnamese refugee is responsible for bringing Sriracha to American consumers

Uncategorized

Electric Truckmaker Rivian, Backed By Amazon, Ford, Raises Whopping $1.3 Billion