It was james carville, an American political strategist, who said, in an oft-repeated turn of phrase, that if he was reincarnated he would like to return as the bond market, owing to its ability to intimidate everyone. Your columnist would be more specific: he would come back as the yield curve. If the bond market is a frightening force, the yield curve is the apex of the terror. Whichever way it shifts, it seems to cause disturbance.

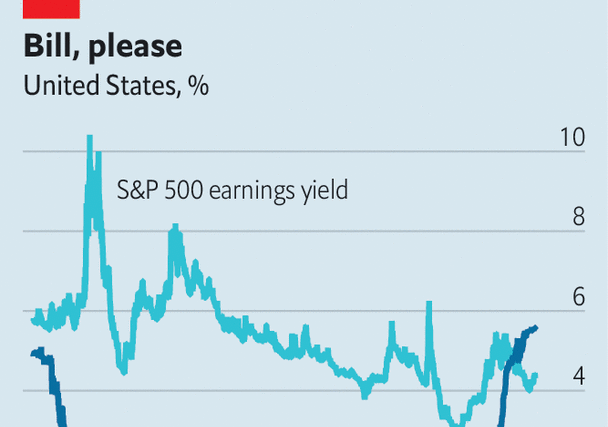

When the yield curve inverted last October, with yields on long-term bonds falling below those on short-term ones, analysts agonised about the signal being sent. After all, inverted curves are often followed by recessions. But now the curve seems to be disinverting rapidly. The widely watched 10-2 spread, which measures the difference between ten- and two-year bond yields, has narrowed markedly. In July two-year yields were as much as 1.1 percentage points above their ten-year equivalents, the biggest gap in 40 years. They have since drawn much closer together, with only 0.3 of a point between the two yields.

Since the inversion of the yield curve was taken as such a terrible omen, an investor would be forgiven for thinking that its disinversion would be a positive sign. In fact, a “bear steepener”, a period in which long-term bonds sell off more sharply than short-term bonds (as opposed to a “bull steepener”, in which short-term bonds rally more sharply than long ones), is taken to be another portent of doom in market zoology.

Driving the latest scare is the rising term premium, which is often described as the additional yield investors require to hold longer-dated securities, given the extra uncertainty over such extended periods. According to estimates by the New York branch of the Federal Reserve, the premium on ten-year bonds has risen by 1.2 percentage points from its lowest level this year, more than explaining the recent surge in long-term yields.

In truth, though, the term premium is a nebulous thing, and must be treated with caution. It cannot be measured directly. Instead, as with a surprising number of important economic phenomena, analysts have to tease it out by measuring more concrete parts of the financial system, and seeing what is left over. Estimating the premium for a ten-year bond requires forecasting predicted short-term interest rates for the next decade, and looking at how different they are from the ten-year yield. What remains—however large or small—is the term premium.

The difficulties do not stop there. John Cochrane of Stanford University’s Hoover Institution points out that, although risk premiums might be more easily estimated at relatively short maturities, the calculations require more and more assumptions about the future of short-term interest rates as analysts move along the curve. When estimates of the term premium are published, they are not typically accompanied by a margin of error. If they were, the margins would get progressively wider the longer into the future the forecast was conducted.

There is also surprisingly little history from which to draw when making assessments of changes in the yield curve or term premium. In the past 40 years, there have been perhaps eight meaningful periods of bear steepening, and only in three of them was the yield curve already inverted. The three instances—in 1990, 2000 and 2008—were followed by recessions, but with widely varying lags.

Movements in bond markets are therefore both easy and difficult to explain. They are easy to explain because any number of factors could be driving yields, including the Fed’s quantitative-tightening programme, concerns about the sustainability of American debt and worries of institutional decay. Yet attributing bond yields to one factor in particular is fraught with difficulty. And without more clarity on the causes of a move, inferring the future from the shape of the yield curve becomes more like reading tea leaves than a scientific endeavour.

One thing is certain, however. Whatever their cause, and regardless of their composition, rising long-term bond yields are terrible news for American companies that wish to borrow at long time horizons, and borrowers who take out new mortgages that will be linked to 30-year interest rates. The effect on the most sensitive borrowers will become only more painful if yields with long maturities remain at such high levels. For anyone concerned about whether a shifting yield curve or a rising term premium signals a looming recession or a nightmare for markets, these simple realities are a better place to start.■

Read more from Buttonwood, our columnist on financial markets:

Why investors cannot escape China exposure (Oct 5th)

Investors’ enthusiasm for Japanese stocks has gone overboard (Sep 28th)

How to avoid a common investment mistake (Sep 21)

Also: How the Buttonwood column got its name

The Most Read

Сryptocurrencies

Bitcoin and Altcoins Trading Near Make-or-Break Levels

Financial crimes

Thieves targeted crypto execs and threatened their families in wide-ranging scheme

Financial crimes

Visa Warning: Hackers Ramp Up Card Stealing Attacks At Gas Stations

News

Capitalism is having an identity crisis – but it is still the best system

Uncategorized

The 73-year-old Vietnamese refugee is responsible for bringing Sriracha to American consumers

Uncategorized

Electric Truckmaker Rivian, Backed By Amazon, Ford, Raises Whopping $1.3 Billion