“Our policy actions work through financial conditions.” So said Jerome Powell, chairman of the Federal Reserve, late last year, referring to the causal chain of monetary policy. As interest rates rise, tighter financial conditions lead companies and consumers to cut spending, prompting economic slowdown and lower inflation. The past ten days have illustrated a less desirable causal chain: from higher rates to a banking crisis.

These stormy financial conditions pose a dilemma for the Fed. Should it remain focused on high inflation, and thus continue to raise rates? Or is financial stability now the priority?

On March 22nd, at a regular monetary-policy meeting, policymakers will decide. Before the turmoil that started with a run on Silicon Valley Bank, a ninth straight rate rise seemed a foregone conclusion. The debate had been whether the Fed would opt for a quarter-point increase, as in January, or a half-point increment. Now there is uncertainty about whether it will raise rates at all. Market pricing assigns probabilities of roughly 60% to a quarter-point increase and 40% to the Fed staying put—not far from a coin flip.

The case for a pause rests on two arguments. First, higher rates are at the root of the financial chaos. Even if Silicon Valley Bank was an outlier in its missteps, other banks and financial firms, from hedge funds to insurers, have hefty mark-to-market losses on their bond holdings. A further rise in rates might add to their notional losses.

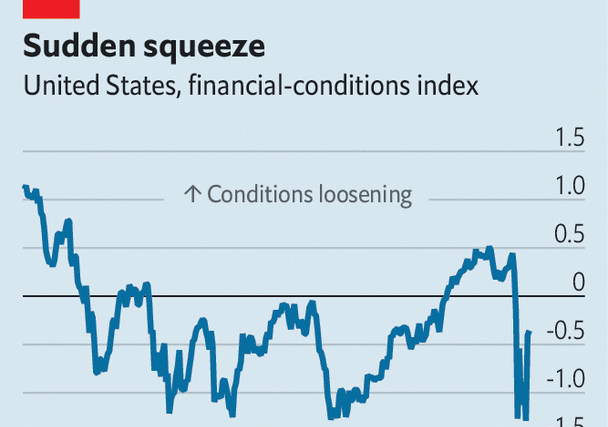

Second, instability is itself a drag on the economy. As confidence cracks, firms try to preserve capital. Banks lend less and investors pull back. Measures of financial conditions—which include interest rates, credit spreads and stock values—have tightened sharply in the past ten days. Eric Rosengren, a former president of the Fed’s Boston branch, has compared it to the aftermath of an earthquake. Before resuming normal life, it is prudent to see whether there are aftershocks and buildings are structurally sound. A similar logic applies to monetary policy after a financial shock. “Go slow, check for other problems,” Mr Rosengren cautioned.

Proponents of pressing ahead with a rate rise accept that financial instability is a form of tightening. But they see this as an argument for a quarter-point rise instead of the half point that many had favoured. Persisting with a rate increase now would signal that the Fed is still intent on quelling inflation, which remains too high for comfort, as illustrated by the 6% year-on-year increase in consumer prices in February. Flickers of a recovery in the property industry indicate that, unlike poorly run banks, much of the economy can endure higher rates.

A rate rise would also demonstrate that the Fed can chew gum and walk at the same time. In an ideal world officials should be able to manage financial stability while keeping inflation in check. With a combination of deposit guarantees, a new liquidity facility and support from bigger banks, a framework is now in place to shore up America’s financial institutions.

The scale of the support is revealed by the size of the expansion in the Fed’s balance-sheet. In the week to March 15th banks borrowed nearly $153bn from the Fed’s discount window, up from less than $5bn in the preceding week, as well as another $11.9bn from the central bank’s new liquidity facility. This has alleviated the sell-off in markets, at least for now, which may give the Fed space to turn its attention back to inflation. Indeed, it can look to the example of the European Central Bank, which on March 16th announced a half-point rate increase, despite the financial chaos.

Then there is the question of market psychology—all the more salient at a time of panic. Counterintuitively, a rate rise may be somewhat reassuring. A pause would suggest that the Fed, hawkish in tone and action for the past year, really is worried. An increase, by contrast, would signal that it thinks the crisis is under control.

Numerically, the difference between the options is small. The Fed is expected either to keep its target for short-term rates to a range between 4.5% and 4.75%, or to lift it to between 4.75% and 5%. In purely financial terms, that is almost immaterial. In terms of policy, it could scarcely be more important. ■

The Most Read

Сryptocurrencies

Bitcoin and Altcoins Trading Near Make-or-Break Levels

Financial crimes

Thieves targeted crypto execs and threatened their families in wide-ranging scheme

Financial crimes

Visa Warning: Hackers Ramp Up Card Stealing Attacks At Gas Stations

News

Capitalism is having an identity crisis – but it is still the best system

Uncategorized

The 73-year-old Vietnamese refugee is responsible for bringing Sriracha to American consumers

Uncategorized

Electric Truckmaker Rivian, Backed By Amazon, Ford, Raises Whopping $1.3 Billion